No, it is not true that most millionaires make over $100,000 a year. In fact, many millionaires have made their wealth through smart investments, business ventures, and financial discipline, rather than relying solely on high incomes. It’s important to note that having a high income does not guarantee wealth, as it is your ability to save, invest, and manage your money effectively that ultimately determines your financial success.

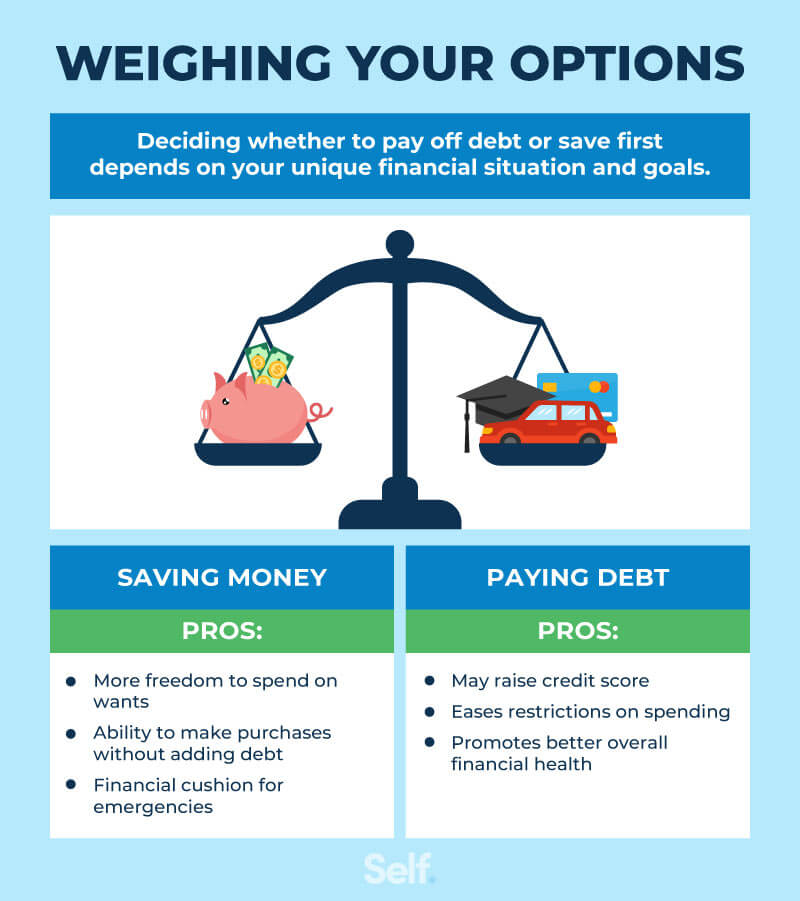

Should I pay off debt or save right now

You will rarely be able to earn more on your savings, than you'll pay on your borrowings. So, as a rule of thumb plan to pay off your debts before you start to save.

Should I prioritize paying off debt

Start chipping away at your highest-interest debt first.

Use any extra money you can find to pay down your highest-interest debt. Every dollar counts. Once you pay off that credit card or other high-interest debt, you'll have more money at the end of the month to put toward the debt with the next-highest interest rate.

Cached

What type of debt should be paid off first

Which Debt Should You Pay Off First Let's cut straight to it: If you've got multiple debts, pay off the smallest debt first. That's right—most “experts” out there say you have to start by paying on the debt with the highest interest rate first.

Cached

Do millionaires pay off debt or invest

They stay away from debt.

Car payments, student loans, same-as-cash financing plans—these just aren't part of their vocabulary. That's why they win with money. They don't owe anything to the bank, so every dollar they earn stays with them to spend, save and give!

What is the 50 30 20 rule

One of the most common types of percentage-based budgets is the 50/30/20 rule. The idea is to divide your income into three categories, spending 50% on needs, 30% on wants, and 20% on savings. Learn more about the 50/30/20 budget rule and if it's right for you.

What is the smartest debt to pay off first

Highest-interest debt

If the goal is to reduce interest, it could help to pay off the debt with the highest interest rate first. If this is your plan, it may help to keep this in mind: If the debt with the highest interest rate is also your largest balance, it may take a while to pay it off.

What are the 3 biggest strategies for paying down debt

Tips for paying off debtStick to a budget. Whatever strategy you choose for paying off debt, you'll need a budget.Start an emergency savings account. There's nothing like an unexpected car repair coming to ruin all your plans to get out of debt.Reduce monthly bills.Earn extra cash.Explore debt relief options.

Is it true that most millionaires make over $100 000 a year

Choose the right career

And one crucial detail to note: Millionaire status doesn't equal a sky-high salary. “Only 31% averaged $100,000 a year over the course of their career,” the study found, “and one-third never made six figures in any single working year of their career.”

What debt is unforgivable

1. WHICH DEBTS ARE NEVER FORGIVEN Bankruptcy never forgives child and spousal support or alimony, criminal fines and restitution, and claims from drunk driving accidents.

What is the 50 15 5 rule

50 – Consider allocating no more than 50 percent of take-home pay to essential expenses. 15 – Try to save 15 percent of pretax income (including employer contributions) for retirement. 5 – Save for the unexpected by keeping 5 percent of take-home pay in short-term savings for unplanned expenses.

How much savings should I have at 30

The general rule of thumb is to have at least six months' worth of income saved by age 30. This may seem like a lot, but it's important to remember that life is unpredictable, and emergencies happen. If you lose your job or get sick, you'll be glad you have that savings cushion.

Is $30,000 in debt a lot

Many people would likely say $30,000 is a considerable amount of money. Paying off that much debt may feel overwhelming, but it is possible. With careful planning and calculated actions, you can slowly work toward paying off your debt. Follow these steps to get started on your debt-payoff journey.

Is $5,000 debt a lot

About 52% of Americans owe $2,500 or less on their credit cards. If you're looking at $5,000 or higher, you should really get motivated to knock out that debt quickly. The sooner you do, the less money you'll lose to interest.

Is $20,000 debt a lot

“That's because the best balance transfer and personal loan terms are reserved for people with strong credit scores. $20,000 is a lot of credit card debt and it sounds like you're having trouble making progress,” says Rossman.

How can I pay off $50000 in debt in one year

What it takes to pay off $50,000 in debt in one year in 5 stepsThe benefits of paying off all your debt in a year.Tips to pay off $50,000 of debt in a year.Create a budget and track all expenses.Be mindful of debt fatigue.Prioritize paying high-interest debt first.Get a higher-paying new job.Freelance on the side.

What salary is considered very rich

Based on that figure, an annual income of $500,000 or more would make you rich. The Economic Policy Institute uses a different baseline to determine who constitutes the top 1% and the top 5%. For 2021, you're in the top 1% if you earn $819,324 or more each year. The top 5% of income earners make $335,891 per year.

What percentage of Americans have a net worth of $1000000

Key points. There are 5.3 million millionaires and 770 billionaires living in the United States. Millionaires make up about 2% of the U.S. adult population. While an ultra-high net worth will be out of reach for most, you can amass $1 million by managing money well and investing regularly.

Which debt dies with you

No, when someone dies owing a debt, the debt does not go away. Generally, the deceased person's estate is responsible for paying any unpaid debts. When a person dies, their assets pass to their estate. If there is no money or property left, then the debt generally will not be paid.

What is the highest debt someone has

Former Société Générale rogue trader Jérôme Kerviel owes the bank $6.3 billion. Here's what his case tells us about financial reform.

What is the 50-30-20 rule

One of the most common types of percentage-based budgets is the 50/30/20 rule. The idea is to divide your income into three categories, spending 50% on needs, 30% on wants, and 20% on savings. Learn more about the 50/30/20 budget rule and if it's right for you.

What is the 50 %/ 30 %/ 20 rule How does it work

The rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must-have or must-do. The remaining half should be split up between 20% savings and debt repayment and 30% to everything else that you might want.

Is 100k in savings good at 30

That's pretty good, considering that by age 30, you should aim to have the equivalent of your annual salary saved. The median earnings for Americans between 25 and 34 years old is $40,352, meaning the 16 percent with $100,000 in savings are well ahead of schedule. How much should you have stashed away at other ages

Is 100k in savings a lot

But some people may be taking the idea of an emergency fund to an extreme. In fact, a good 51% of Americans say $100,000 is the savings amount needed to be financially healthy, according to the 2022 Personal Capital Wealth and Wellness Index. But that's a lot of money to keep locked away in savings.

How much debt is unhealthy

Debt-to-income ratio targets

Generally speaking, a good debt-to-income ratio is anything less than or equal to 36%. Meanwhile, any ratio above 43% is considered too high.

What is an OK amount of debt

A common rule-of-thumb to calculate a reasonable debt load is the 28/36 rule. According to this rule, households should spend no more than 28% of their gross income on home-related expenses, including mortgage payments, homeowners insurance, and property taxes.